The Ultimate Guide to Hail Roof Inspections: Tips and Techniques

Hailstorms can wreak havoc on your home, particularly your roof. Even seemingly small hailstones can cause significant damage over time. That’s why inspections right after a storm are crucial to ensuring the structural integrity of your roof.

In this comprehensive guide, we will walk you through the essential tips and techniques for conducting a thorough hail roof inspection checklist as a Homeowner.

Table of Contents

Understanding Hail Damage

Before diving into the inspection process, it’s essential to understand how hail can affect your roof. Hail damage isn’t always immediately apparent. Small dents and granule loss might seem insignificant at first, but they can lead to more extensive problems over time, including leaks and weakened structural integrity.

Hail damage can significantly impact roof shingles in various ways:

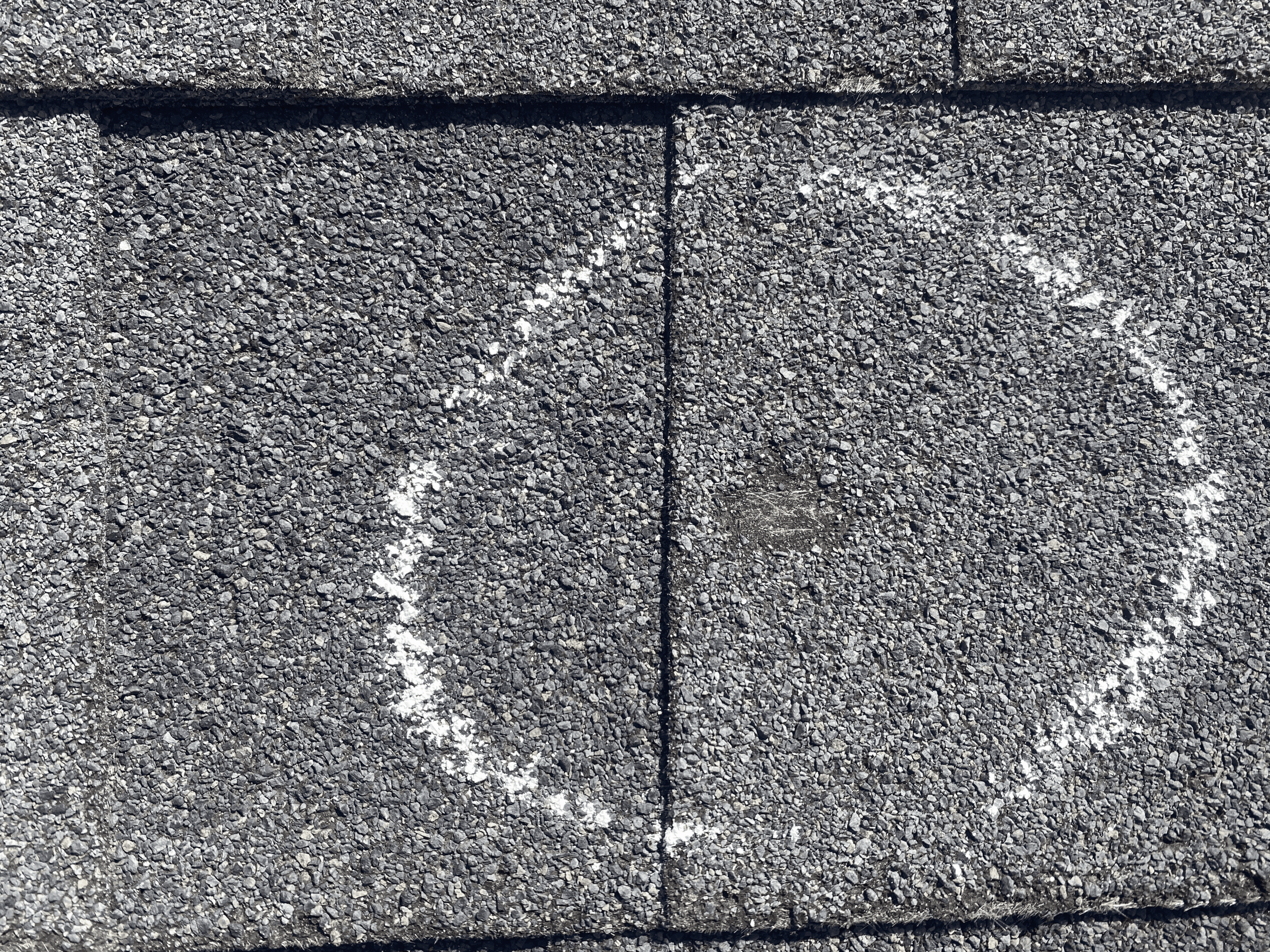

Bruising or Denting: Hailstones can create dents or bruises on shingles, which might not be immediately visible. Over time, these weakened areas can lead to further deterioration.

Granule Loss: The impact of hail can dislodge the granules from the surface of the shingles. These granules protect the asphalt layer underneath from sunlight and weathering. Loss of granules can accelerate the aging of the shingles.

Cracking: Large or high-velocity hailstones can crack shingles, leading to immediate and obvious damage. Cracked shingles can allow water to seep through, leading to leaks and water damage.

Loosening of Shingles: The impact of hail can loosen or displace shingles, compromising the roof’s integrity and making it more susceptible to wind damage and leaks.

Compromised Waterproofing: Any damage to the shingles can potentially compromise the waterproofing effectiveness of the roof, leading to water infiltration and associated problems.

Timing Matters

Timing is crucial when it comes to hail roof inspections. Ideally, you should perform an inspection after every significant hailstorm. However, if you’re unable to do so immediately, it’s never too late to check for damage.

We do not advise any of our homeowners to get up on the roof to perform an inspection. Leave that to our trained professionals at HHH Roofing & Construction.

When is Hail Season in Texas?

Hail season in Texas typically occurs during the spring and early summer months, with the highest likelihood of hailstorms from March to June. This is when warm, moist air from the Gulf of Mexico can collide with cooler air masses, creating the conditions necessary for severe thunderstorms and hail formation.

Keep in mind that Texas is a large state, and the timing and intensity of hailstorms can vary depending on the specific region within the state. It’s always a good idea to stay informed about weather conditions and to be prepared for severe weather events, especially during the spring and early summer months.

Step-by-Step Inspection Process

In order to file an insurance claim for hail damage, you’ll need a professional evaluation from a licensed roofing company. For the sake of safety, it isn’t recommended to climb on your roof – especially if it may be compromised by a serious weather event. However, you may be able to spot hail damaged without having to fetch a ladder.

1. Safety First

Always prioritize safety. Before inspecting for hail damage, ensure that it’s safe to do so. Wait until the storm has completely passed and it’s safe to be outside.

2. Check Exterior Surfaces

Roof: Start by examining your roof. Look for signs of damage on shingles, especially along the ridges and edges. Look for dents on metals, vents, & chimneys. You might notice even large enough hail will crack skylights.

Siding: Check the siding of your home for dents, cracks, or holes. Hail can cause visible damage to all types of siding materials (vinyl, James Hardie, or metal). It can be simple as a dent or even extreme to completely going through the material.

Windows: Especially second story windows that have screens will be the most visible for identifying hail damage: Screens will be damaged and have holes through them. Also, check for dents or dings in the window frames.

{kind=link}

{kind=link}

3. Gutters and Downspouts

Hailstones can cause dents and damage to gutters and downspouts. Look for obvious signs of impact.

4. Outdoor Equipment and Fixtures

Air Conditioning Units: Check your outdoor HVAC unit for signs of dents or damage from hail. It will mostly damaged the condenser coils.

Fences, Decks, and Porches: Examine these outdoor structures for any signs of hail damage, such as dents, cracks, or splintered wood. It usually will take at least 2″ hail or bigger at high winds to damage these structures.

5. Vehicles and Personal Property

If your car was outdoors during the hailstorm, check it for dents, cracks in the windshield, and other signs of hail damage. Similarly, inspect any other personal property that might have been exposed to the storm.

6. Document the Damage

- Take clear photographs or videos of any hail damage you find. These images can be useful for insurance claims and repair assessments.

- Make detailed notes about the extent of the damage. This can help when communicating with insurance adjusters and contractors

7. Contact your Insurance Company

If you find significant hail damage, contact your insurance company as soon as possible to report the damage and start the claims process. Provide them with the documentation you gathered.

8. Seek Professional Assessment

Consider hiring a professional contractor or a roofing expert to conduct a thorough inspection. They can provide a more detailed assessment of the damage and offer repair or replacement recommendations.

Remember that it’s important to address hail damage promptly to prevent further deterioration and potential leaks. Always consult with professionals if you have any doubts about the extent of the damage or the necessary repairs.

Conclusion

Regular hail roof inspections are essential for maintaining the integrity of your home. By following these tips and techniques, you can identify and address hail damage promptly, preventing further issues down the line. Remember, safety should always be your top priority, so exercise caution when inspecting your roof. If in doubt, seek professional assistance to ensure the longevity of your roof and the safety of your home.

What to Do After a Hailstorm in Houston Texas

Hailstorms can cause significant damage to our homes, particularly to roofs, windows, and siding. In this blog post, we’ll provide you with essential steps to take after a hailstorm, including assessing the damage and contacting your insurance company, to help you navigate the recovery process smoothly and restore your home’s condition.

Table of Contents

Assess the Damage

Once the hailstorm has passed, it’s important to assess the damage to your home.

As a homeowner start by:

- Visually inspect the exterior of your property, paying close attention to the roof, windows, and siding.

- Look for signs of dents, cracks, or holes caused by hailstones.

- Check the condition of your windows for any shattered or broken glass.

- Examine the siding for any visible damage, such as cracks or punctures.

- Inspect the surrounding area for fallen branches or debris that may have caused additional damage.

It’s a good idea to document the damage with photographs or videos, as this can serve as valuable evidence when filing an insurance claim.

Request a Roof Inspection

It is important to get a roofing company out to your roof to assess the damage as soon as possible. A roofing company is more equipped to answer any questions or concerns you may have regarding the extent of the hail damage.

A roofing company will complete a storm damage roof inspection. This will include looking at the following:

- Dents to Gutters/Downspouts

- Hail Dents on Metal Flashings

- Hail Dents on pipe flashing/roof vents

- Hail Damage to the Shingles

Contact Your Insurance Company

Promptly reporting the hailstorm damage to your insurer is vital in initiating the claims process and ensuring that you receive the necessary assistance for repairs and restoration.

Here are some important guidelines to follow when contacting your insurance company:

- Report the hailstorm damage promptly

- Provide accurate and detailed information

- Follow the claims process as instructed

- Keep records of all communication

- Be aware of your policy coverage and deductible

What Makes Hail So Damaging?

Hail can be highly damaging due to its size, density, impact force, repetitive strikes, wind-driven trajectory, and the vulnerability of certain materials. Hailstones come in various sizes, and larger ones carry more force when they fall, leading to significant impact damage. During a hailstorm, multiple hailstones can repeatedly strike the same area, causing cumulative effects and weakening structures.

Is It Necessary To Fix Roof Hail Damage?

The overall answer is yes. Hail striking your roof can compromise the integrity of your roof. Even if there are no visible leaks, over time leaving the damage unattended can cause long-term damage.

Do you think you have hail damage?

What To Do If You Have Missing Shingles

A well-maintained roof is a crucial part of your home that many homeowners should be aware of. It is important to keep an eye out for any possible signs that your roof may be in need of extra care such as repairing those missing shingles.

In this blog post, we will explore what you should do if you missing shingles. We will help answer your questions, such as, should I replace my whole roof? or what should I do next after I see a missing shingles on my floor.

Table of Contents

How To Know If There Are Missing Shingles On My Roof?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Step One: Hire a Roofing Company

First, it is important to hire a roofing company to come out to your home to assess the condition of your roof, give an estimate and help guide you through the process.

A roofing company will help you:

- Assess the damage

- Give you an estimate

- Help you decide between a full replacement or a repair

- Help assess whether or not you should file an insurance claim.

Step Two: Decide Which Option is Best for You: Full Roof Replacement or Repair?

A Roofing company will help aid you in your decision of deciding which option is right for YOU!

Deciding is up to these factors:

- Assess the extent of the damage to determine if repairs are sufficient.

- Consider the age of the roof and if a replacement is more cost-effective in the long run.

- Compare the cost of repairs versus replacement, factoring in long-term savings and benefits.

- Evaluate your future plans for the property, such as selling or staying long-term.

- Review any existing warranties on the roof to determine coverage for repairs or replacement.

- Seek the advice of a professional roofing contractor for a comprehensive assessment and recommendation

Carefully evaluate the pros and cons, consider the long-term benefits, and consult with roofing professionals to guide you toward the most suitable choice for your home and budget.

Step Three: Decide if You need To File An Insurance Claim?

If you’re facing significant roof damage that may require repairs or a replacement, filing a roofing insurance claim can help you alleviate the financial burden, especially after a storm.

Here we outlining the steps to take when filing a roofing claim:

- Review Your Insurance Policy:

- Document the Damage:

- Contact Your Insurance Company:

- Schedule an Inspection:

- Obtain Repair Estimates:

- Keep Records:

- Follow Claim Filing Procedures:

- Be Prepared for an Adjuster’s Evaluation:

- Review the Settlement Offer:

- Proceed with Repairs or Replacement:

Common Question Many Homeowners Ask

Will My Roof Leak if I Have Missing Shingles?

Yes, Missing shingles on your roof can lead to leaks and water damage over time, emphasizing the importance of timely repairs or replacement to maintain the structural integrity of your home.

How Do I Know if My Roof Shingle Is In Bad Shape?

You can determine if your roof shingle is bad by looking for signs such as curling, cracking, missing granules, or significant wear and tear, which can indicate the need for repair or replacement.

Does Homeowners Insurance Cover Shingles Blown Off Roof?

In Texas, homeowners insurance generally covers shingles blown off the roof due to wind or severe weather, but it’s important to review your policy and consider factors such as deductibles and coverage limits to determine the extent of the coverage.

do you need your missing shingles replaced?

5 Most Common Roof Insurance Questions

These are the 5 most common roof insurance questions we get asked by homeowners when they have storm damage.

1. What is the Insurance Company Looking For?

When you file an insurance claim, your insurance company will send out an adjuster to inspect the damage. The insurance adjuster is looking for physical evidence for storm damage either Hail or Wind damage.

Hail Damage

Wind Damage

The insurance adjuster looks for “hail hits” on your shingles, exposing the underlayment or fiberglass or if it’s wind damage they will look for missing shingles and lifted shingles. They will need to find enough evidence on your roof to declare that it had enough damage to the point of shortening the standard roof lifespan.

Even though hail damage doesn’t pose an immediate threat to your home, it will eventually lead to problems.

- Accelerated Granule Loss

- Accelerated Roof Aging

- Void Manufacturer’s Warranty

2. Will My Insurance Rates Go Up if I File a Claim?

No, your rates will not go up if you file an insurance claim!

This is due to the storm damage happening as an “act of God”. It is completely out of your control and there was nothing you can do to prevent it.

Insurance rates can increase for everyone in a certain area due to a major storm passing through & multiple claims are being filed. Remember, this happens to everyone even those who haven’t filed any claims.

3. How Does The Payment Process Work?

Once the insurance claim is approved, the insurance company will send over the 1st check. This 1st check is used to get started on your work. As soon as the job is complete, you will send the invoice from the roofing company or proof of completion. The insurance company will then send the 2nd check.

First check

The first check will be sent to the policyholder from the insurance company as soon as the claim has been approved.

Second Check (Recoverable Depreciation)

The second check is withheld until the repairs to your roof are completed. The second check is generally a percentage of the total amount and is usually referred to as “recoverable depreciation”. It is sent to the policyholder when the insurance company receives an invoice for the final payment.

4. Can I Have My Deductible Covered?

No, you cannot have your deductible covered! A deductible is part of your home insurance policy. It is illegal for contractors to waive your deductible.

How would a contractor help me avoid paying a deductible?

One way is by “creating extra costs” giving you a higher estimate than the actual cost to repair your roof. The contractor then uses the extra money paid by the insurance company to cover your deductible. That is illegal.

What's the harm?

Contractors who waive your deductible will be sending false information to your insurance company about the cost of repairs. That would be insurance fraud.

In our experience, these contractors will make their profit by cutting corners or using lower-quality products.

How will the insurance company know if I paid my deductible?

Insurance companies can ask for proof that you paid your deductible before they send the 2nd check. You might have to show a check, money order, credit card statement, or a copy of the payment plan with your contractor.

5. Do I Need to Get Multiple Estimates?

Yes & No

I recommend getting multiple estimates to shop for the right roofing company that is licensed & local to explain the process to you and maintain great communication.

Sometimes insurance companies will ask the homeowner to shop around for 3 bids. 90% of the time insurance companies will underpay your roof claim. A great roofing company will create a bid using the Insurance company estimate software, Xactimate to provide an accurate estimate using the updated monthly local pricing.

Using a great roofing company, won’t make you pay more of a deductible it will only solidify that you have the best experience and a High-Quality New Roof.

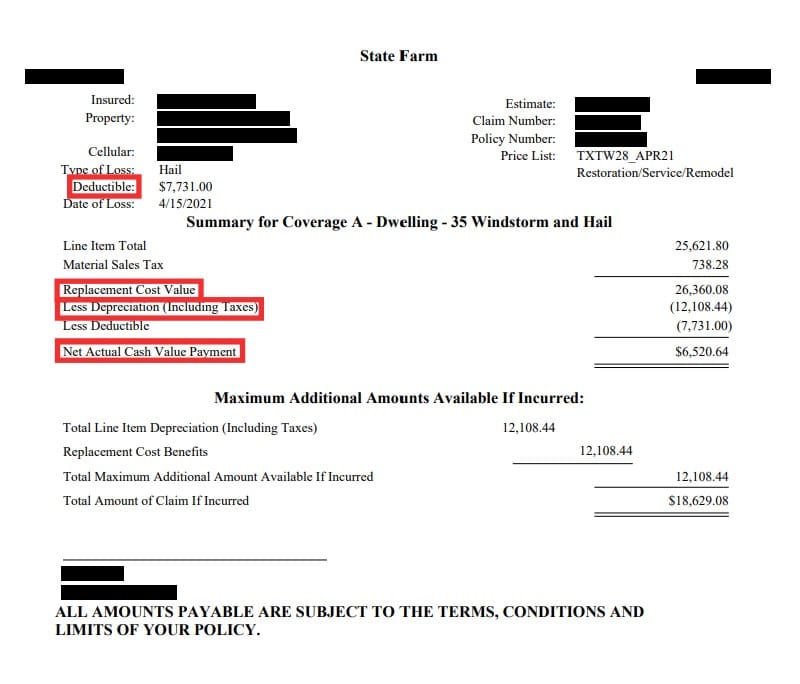

How To Read An Insurance Estimate

How to Read An Insurance Estimate? Did you have recent storm damage to your home? You called your insurance company to file a claim and had an Insurance Adjuster come out to review the damage.

Great News! You got approved and received an Insurance Claims Report to cover the repairs. As you look over the estimate you have these common questions:

- What is RCV?

- Depreciation Explained

- What is ACV?

- What’s my Deductible?

- What’s the Difference between RCV & ACV?

NOTE: In 2022, we have seen an unprecedented labor shortage as a side effect of the COVID-19 pandemic. The demand for materials has skyrocketed. As a result, materials prices have been changing almost monthly (about 5-7% increases).

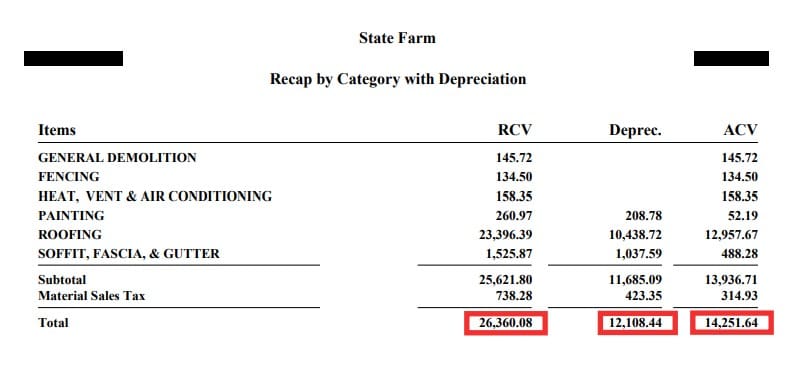

Below we will use a Real-life Example of an Insurance Claims Report from State Farm from April 2021. We have made sure to blur out all personal information.

We are not by any means Insurance professionals just a Roofing Company that has seen/written many Xactimate estimates and want to share our knowledge & point of view as a roofing contractor.

What is Xactimate?

The insurance industry primarily uses software called Xactware to format insurance estimates. The specific program is called Xactimate.

Xactware maintains fair market pricing for both materials & labor adjusted to each city or region-specific pricelists updated monthly.

It’s a way for an Insurance Company & Contractors to agree on pricing.

Xactimate Terminology

RCV (Replacement Cost Value)

The total amount that your insurance company has estimated as the cost of repairs to your property.

Depreciation

The insurance company will apply depreciation to your damaged property based on the product’s age and “life expectancy”. The decrease in the value of the property over a period of time due to wear, tear, and condition

Let’s say you have a roof that lasts 30 years and it has been 15 years since the roof was installed. That means 1/2 of its lifespan has been depreciated because over time it loses its condition.

Deductible

This is your share of the cost of the repairs. Legally, this amount is your responsibility to pay your contractor.

ACV (Actual Cash Value)

The amount that your insurance company has estimated as the cost of repairs TODAY, includes depreciation.

ACV =

RCV – (Depreciation + Deductible)

Recoverable Depreciation

If your claim has recoverable depreciation, that is money you will receive after you have incurred the costs of the repairs.

If you have Replacement Cost Value coverage in your policy, your depreciation should be “Recoverable”.

Non Recoverable Depreciation

If your insurance coverage is Actual Cash Value, then the amount of the depreciation will be Non-Recoverable. This means you will not receive the depreciation amount as part of the claim, so your share of the cost of repairs will be much higher.

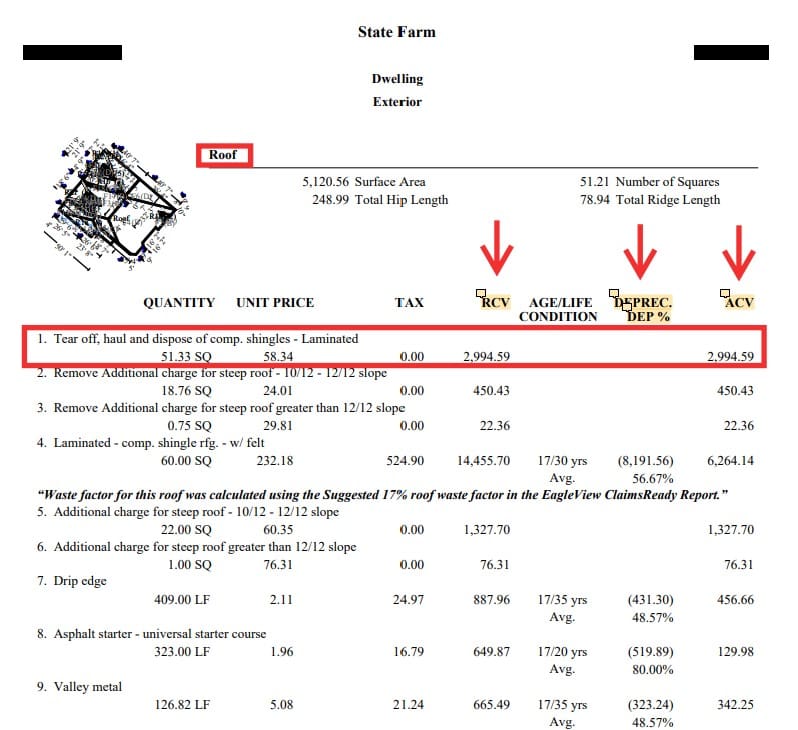

Breakdown of Estimate (Roof Section)

Line Items

Replacement Cost Value

Depreciation

Actual Cash Value

Category

When we are hired by you as the roofing contractor our main focus is making sure every LINE ITEM is included by the Insurance Company to complete a proper restoration of your roof in accordance with local codes.

Example:

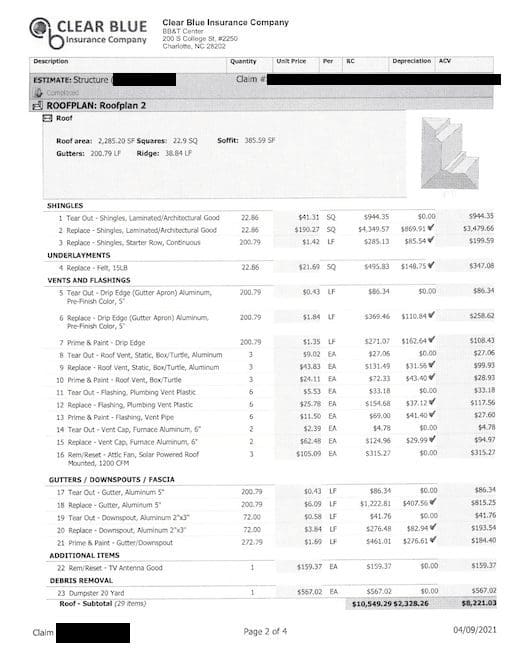

Let’s look at the Drip Edge at Line Item #7.

As a roofing contractor, we will replace the 409 Linear Feet of Drip Edge of your home. Every foot of Drip Edge costs (Material & Labor) $2.11.

Replacement Cost Value=$887.96

Depreciation=$431.30

Actual Cash Value=$456.66

The actual Replacement Cost is $887.96 but since the roof is 17 years old it has depreciated $431.30 so Today’s Actual Cash Value is $456.66.

Summary With Multiple Categories

We love using this insurance claims report because it has multiple categories & shows you the breakdown for each trade.

As the roofing contractor, our replacement cost value to replace your roof is $23.396.39.

The total to restore this home from Hail Damage is $26,360.08 based on Xactimate pricing & correct line items. Since the home is older & it has normal wear & tear the depreciation is $12,108.44. In turn, the actual cost to restore the home based on its condition is $14,251.64.

Should I File An Insurance Claim For My Roof?

We got a lot of questions about roof insurance claims. Like should I file an insurance claim on my roof? You maybe have door knockers or people pressuring you to file an insurance claim but you don’t know who to trust. The short answer is yes you should file a claim on your roof if there is storm damage. Read below or watch to video to see why we recommend filing a claim.

What Type of Storm Damage Would you Suggest Filing A Roof Claim For?

- Hail

- High Winds

- Tree Falling and Damaging Your Roof

- Hurricane

If there has been a recent storm in your neighborhood or you notice your roof is damage that’s a good sign you should consider filing a claim. Before you call your insurance company we recommend calling your local roofer to come out and see if there is actual storm damage.

Reasons Why You Should File An Insurance Claim For Your Roof

1. Your Roof Has Storm Damage

If there has been a storm then your roof may be damaged. The reason why insurance companies cover hail, high winds, natural disasters, etc. is because the lifespan of your roof has been shortened. If your roof has hail damage the granolas have fallen off or even have holes on the shingle. If there is high wind the sealant is gone.

Your roof may seem fine to the average person but if you can’t know for sure until you walk on the roof and inspect everything. If your roof is damaged then you may not notice but you’ll start having leaks a lot sooner than you should be having.

Signs of Storm Damage

- Granules Missing

- Bruised Shingles

- Dented Metals

- Lifted Shingles

{kind=link}

{kind=link}

{kind=link}

2. You Are Paying For The Storm Damage Already

If you home insurance, chances are you have been paying the premium for years. You are paying for protection for a reason. If your neighbors roof gets replaced and you decide not to file a claim, your rates are probably going to go up and you will have to replace your roof out of your pocket. If there is storm damage file a claim because you are already paying for it. Why pay for insurance if you’re not going to use it when you have storm damage on your home.

3. You Have Nothing To Lose If you File A Roof Claim

Please note only file a claim if you sincerely think there is storm damage and always call a roofer first. A lot of times homeowners think filing a insurance claim on their roof is going to make your rates go up. No your rates do not go up because it is an “act of god” meaning you had no control over the storm. It’s not your fault and that’s why your insurance covers it. Worse case scenario if you file a claim and do not have storm damage than at-least you have peace of mind and now have a better understand of the condition of your roof and your policy contract. You have nothing to lose if you file a claim but if you don’t it may cost you in the near future.

BONUS: If You Don’t Use Your Insurance You Lose It

Sometimes homeowners think I’ll file a claim later. Or they aren’t aware they have storm damage. If you don’t file a claim within a certain time period from the date of the event (usually 2yrs) your insurance will not cover it anymore. Or if you change insurance companies and your new insurance company is telling you, you have to replace your roof. Even if you have hail damage you have to pay it out of pocket because you canceled or changed your policy holder.

We know insurance claims can be confusing. If you have any other questions or think you might have storm damage, give us a call. We are a Local Roofing Company located in Spring, TX. We are here to help make the process easier for you and give you peace of mind.

5 Step Roof Insurance Claim Process 2021

Is your roof damaged? Maybe there was high winds, hail, or even a hurricane that came by. Either way we know when it comes to the roof insurance claim process it can be very confusing and intimidating. You might have door knockers, companies calling you, direct mail etc. That’s why we made this blog to help you understand the process so you do not get taken advantage of.

Insurance Claim Process into 5 Easy Steps

- Notice Stage

- Inspection Stage

- Insurance Claim Stage

- Scope of Work

- Roof Replacement

STEP 1: Notice Stage

As soon as you see any sort of storm damage document as much as you can. Take pictures of everything you see whether it is the actual hail falling, broken windows, missing shingles, etc. Storm damage can come from Hail, High Winds, Tornadoes, Hurricanes, etc. Most importantly roving damage is essential for your insurance claim.

{kind=link}

{kind=link}

STEP 2: Inspection Stage

Your insurance company will likely ask you to call a local roofing company to inspect your roof. You might have door knockers coming to offer services or you might see yard signs everywhere of roofing companies. Above all we recommend going to google and searching for a local roofing company. Do your research in picking the right roofing company as you will likely go through the process with them if you do have storm damage.

Quick Checklist Before You Hire A Roofing Company:

- Local to your area

- They have been in business for years

- Have an online presence

- Check for good Google reviews

- Preferably Licensed & Insured

- A+ BBB Rating

That roofing company will come out and do a roof inspection. If they find significant hail or wind damage to your roof they will explain the process and tell you to call your insurance company to file a claim. Your insurance company will give you a claim number and a time a insurance adjuster will come out to your house. Give all that information to your roofer.

Sometimes a roofing company will have a contingency agreement. It is basically a contract stating they are representing your best interest and it gives them permission to talk to your insurance provider and give all necessary documents. And if your insurance claim is approved they are the ones that will do the job.

Contingency agreements protect contractors and it will not hurt you. That’s why we recommend doing your research on a roofer first. If a doorknocker comes to your home and you do not feel comfortable we do not recommend signing a contingency agreement.

{kind=link}

{kind=link}

{kind=link}

STEP 3: Insurance Claim Stage

Once you call your insurance company they will start the claim process and have an adjuster come out. The adjuster will come out and do full inspection and report on your property. It is best to have your roofer come out there at the same time. The roofer is there to help the adjuster and make sure everything is accounted for and they are on the same page.

Afterwards the adjuster will talk to you and turn in the report. They will likely submit everything to the desk adjuster and they will determine whether to accept your claim or not. If accepted you will get a packet of papers through the mail. It will explain your insurance policy, damaged covered, and what they are paying. It can be confusing if you have never done an insurance claim. That’s why it’s important to choose the right roofer to help explain the paperwork.

{kind=link}

STEP 4: Scope Of Work

When you review the insurance claim report go over the scope of work with your roofer. The insurance company will likely use a software called xactimate to create the scope of work. It will have everything itemized down to the quantity. However at times the xactimate is incomplete and is missing line items. Your roofer is doing the work that the insurance company authorizes. So its best to make sure everything you need is included.

STEP 5: Roof Replacement

Once everything on the scope looks fine your insurance company will send you your first check. Talk to your roofer to schedule the job. You will give the first check to your roofer along with the deductible that you owe. As soon as the job is completed and you are satisfied with the work. Your roofer will send the last invoice along with any other documentation your insurance provider asks for to release the last check. Once you receive the last check give that your roofer and that is it. You have a new roof now.

{kind=link}

{kind=link}

{kind=link}